Three Tax Strategies For The End of 2017

By: Gregory L. Cartwright

Now that the The Tax Cuts and Jobs Act (“Tax Act”), has been signed into law, we are beginning to get a clearer picture of what 2018 will look like for many of our clients who are small business owners or self-employed. And, while much more analysis will need to be done in the coming months, a few strategies are already emerging. Here are three relatively simple strategies you should be considering now to put you in the best position possible for 2018.

1. Delay receipt of income until 2018.

The impact of the tax bill will vary widely from taxpayer to taxpayer. However, in general terms, the vast majority of taxpayers should see some reduction in their tax obligations moving forward. The effect of this is that income in 2018 will be taxed at a lower rate than in 2017. Accordingly, to the extent you can, you should try to time the recognition of income so that it is received in 2018 when your tax rates will be generally lower. There are right ways and wrong ways to time your income, so be sure to check with your tax accountant to ensure you are doing it correctly.

2. Make your expenses in 2017

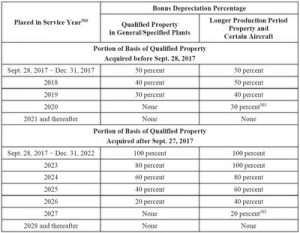

The corollary of delaying your income until 2018, is to try to expense as much as you can now in 2017. The Tax Act makes significant changes to the bonus depreciation rules. Most importantly, it increases the “bonus depreciation” amount from 50% to 100%, and not only makes that bonus deprecation amount retroactive to apply to qualified property acquired after September 27, 2017 but even changes the rules to apply to used property as long as it is new to the taxpayer. A chart included in the Conference Agreement on the Tax Act demonstrates how these changes should be applied.

An detailed analysis of the tax planning strategies arising from these new depreciation rules is beyond the scope of this post, so if you believe you have an opportunity to take advantage of these rules in 2017, you should be consulting your tax accountant and making qualified purchases before the end of 2017. But, all things being equal, any type of business expense that you might make should be made by the end of this tax year. Simply put, for most taxpayers, the tax benefits of paying for business expenses and making purchases of depreciable property in 2017 will be more advantageous than waiting until 2018. It looks as if Congress has banned the prepayment of some state and local taxes, but it appears that other types of payments incurred in the ordinary course of business should be permitted.

3. Set up a Pass Through Entity in 2018

The changes to taxation of Pass Through Entities is a major part of new tax rules. If you own rental property, run a small business or perform any services where your income is reported on a 1099 (like an independent contractor or outside consultant) operating a Pass Through Entity should provide you with significant tax savings. If you are currently an employee, but are thinking about becoming an independent contractor, now might be the time. There are important differences between being categorized as an employee vs. an independent contractor, so care should be taken in making that decision.

Typically, the Pass Through Entity that will be set up will be either an S-Corp or an LLC, although depending on your particular circumstances a limited partnership, a limited liability partnership or other entity type might be right one for you. Moreover, depending on the type of business or profession, a cap on the amount of income you can treat in this manner will be applied. For example, the tax deduction is phased out for owners of professional services businesses like lawyers and accountants whose taxable income exceeds $315,000 for married individuals filing jointly or $157,500 for individuals. Nonetheless, the use of a Pass Through Entity will still provide significant tax benefits to even those types of businesses.

Regardless of the type of Pass Through Entity you select, by being paid this way, you may be able to be taxed at a rate as low as 20% on that income. We are recommending that clients wait until January to set up such an entity, but that they do so very early in the tax year so as to take full advantage of this new rule. Because of this, you should begin working with your legal and tax advisors now in order to analyze your options and to be ready to move quickly in the new year.

© Copyright 2017 Gregory L. Cartwright. All rights reserved.